How the stock markets story is scripted – Part 1

Indian stock market crashed by around 40% from the highs of January to the lows of March this year. After that we have seen a rally of over 20%. Investors are in a dilemma and split between the two kinds of fears, the fear of missing out but at the same time they have the fear of the market going back to the previous lows and even beyond.

Before we know what lies ahead, we need to understand one very key aspect of the market. In simple terms we know that the market is the play of demand and supply. If the demand is more the stock prices go up and if the supply is more, they go down. But who creates this demand and supply?

The Big Players

The shareholding pattern of our markets is skewed towards the institutional investors. Since 51% of the stake is held by the promoters, we have less than half of the shares available as free-float. Of that remaining free-float shares, the FIIs/FPIs (only referred as FIIs for brevity going forward) and DIIs account for around 60% of the market share.

From the above data it is obvious that FIIs and the DIIs have a lot of influence on creating the demand and supply. What is immediately not obvious is that these two entities normally trade in tandem. If you look at any period of historical data, you would find that when one of them sells the other one buys and vice-versa. In simple terms it means that the share just exchanges hands between FIIs and DIIs and the retail investors offsets any difference left. Of course there are few occasions when both of them are on the same side of the fence. Make a note of this important point as we will talk about it in more detail in a later section.

Subprime Mortgage Crisis

Before discussing the play of institutional investors, we need a reference time period for analysis of the price movement. I have taken the example of the subprime crisis, so we are analyzing the data between 2008 to 2010.

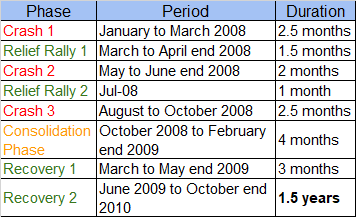

The following chart is the Nifty 50 chart during the subprime crisis period. The overall period starts from January 2008 when the market witnessed the first crash and went on till October 2010 when it came back up to the same levels. For our analysis we have split this entire period into intervals based on the direction of price movement:

For better clarity of the time period refer to the following table which outlines the exact month and overall duration of the price movement.

The Real Story

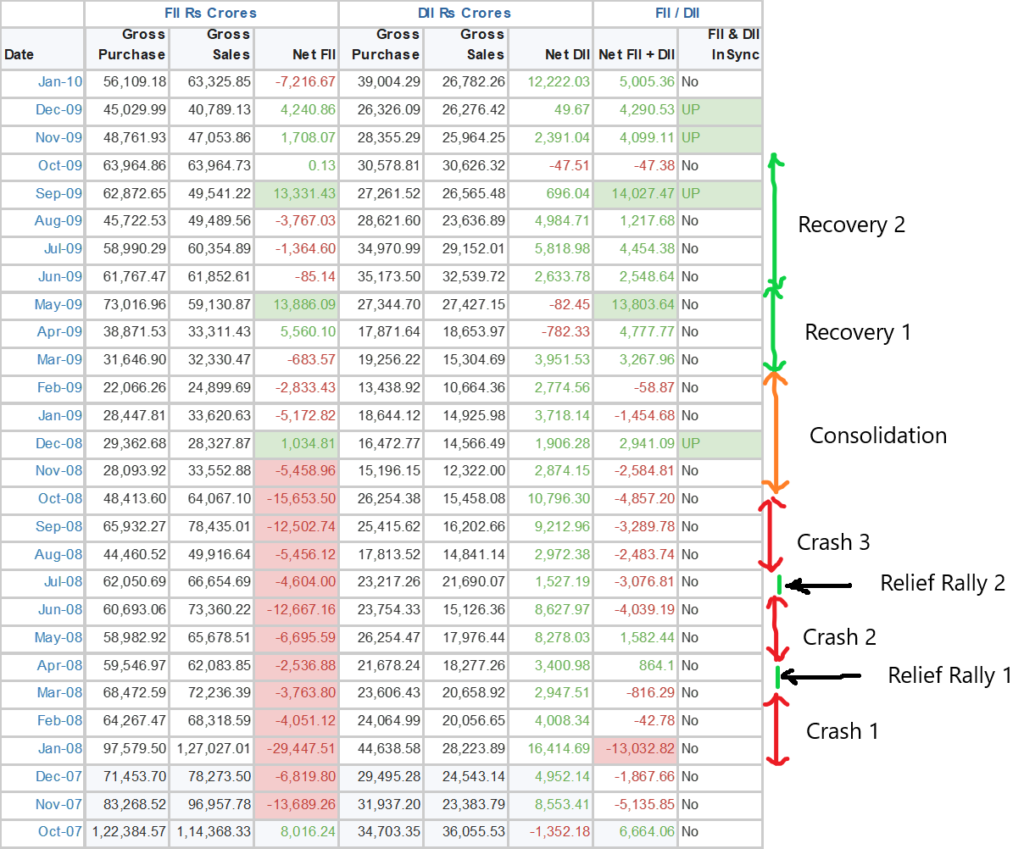

Going back to the earlier point that FIIs and DIIs trade in tandem, check the inflow and outflow data of FIIs and DIIs during the subprime crisis period. Pay attention to the last column. The column highlights in which months both FIIs and DIIs were on the same side. You would notice that in more than 2 years, both were net buyers in a month on only four occasions.

From the above table also notice the huge outflow of 13,689 crores (INR) by FIIs in November 2007. This is where the subprime crisis story started. Four months trailing to that, the net flow of FIIs and DIIs combined was positive. In this month the net flow turned negative to the tune of over 5000 crores.

Come January 2008, the Nifty was comfortably sitting at close to 6300 even though FIIs had pulled out over 20,000 crores in the previous two months. That is when the FIIs dropped the hammer and withdrew close to 30,000 crores from the market. So more than 50,000 crores were taken out of the market and that started the beginning of stock market crash in India.

The FIIs continued to withdraw money from Indian markets for over an year but the market crashed in three tranches. In between we saw the upward price movement twice which was short lived. Investors came back into the market thinking that it is the start of the market recovery but they turned out to be only relief rallies. It heightened the interest of individual investors for a while before taking the market further down.

In that entire one-year period starting November 2007, mostly the net flow of FIIs and DIIs was in negative, Which means this period saw a lot of inflow of the money from individual investors.

In December 2008 we witnessed the return of the FIIs. For the first time in over a year the net flow of FIIs turned positive. The DIIs were also on the same side and they also ended the month in positive. This was a first since April 2007. The overall market sentiments started turning neutral if not positive which arrested the free-fall of the market.

Over the next couple of months, we saw a consolidation phase when the market moved sideways. The FIIs continued to withdraw money but the amount was gradually declining. In March 2009 the FIIs again started investing and the overall month’s outflow ended at few hundred crores only.

The return of FIIs saw the beginning of the recovery phase. Coincidentally in September 2009 we saw a huge inflow of 13,886 crores which was a very similar amount to the outflow we first witnessed in November 2007 when this whole story started. This started the long road to recovery of the Indian stock market.

During this period the rare occurrence of FIIs and DIIs to be on the same side of flow became quite common. Both FIIs and DIIs were ending in positive net flow which meant the retail investors started booking profits from the first phase of recovery and FIIs and DIIs started accumulating the assets for the long term.

Conclusion

This story tells us one very important lesson. The big players value the importance of capital protection more than any other investment rule. Looking for higher returns they do invest in developing economies but sensing any serious distress they rush back towards the safety of US treasury bonds. The individual investors should take a leaf out of the books of such investors and be more prudent in such extraordinary situations. If you lose 15-20% of your capital, you will still live to fight another day but if you lose more than 50% of your capital then it would take a long time to recover from such losses.

Please note, the objective of this blog is to make people aware of the role of institutional investors in market fluctuations as per my interpretation of the subprime crisis data. This is in no way a recommendation to base your investment strategy just on this factor.

If you have found this blog interesting, stay tuned for the upcoming blog analyzing the current market situation.